A Better Way to DCA?

by HunterEverybody and their brother is launching a suite of buffer ETFs. As I’m sure you already know, these strategies generally use options to hedge exposure to broader equity markets and offer (total or limited) downside protection in falling markets with (limited) upside participation in rising markets. Maybe you are squeezing that into your equities portfolio or talking yourself into sliding into your alts allocation already, but I think one area that you can really put these things to work is in DCA plans.

Dollar Cost Averaging (DCA) is the bain of every allocator’s existence. No matter how much you try to talk sense into that client that just cashed in on a windfall business sale, inheritance, or sale of a vacation home, they just won’t listen to reason (which, of course, is that lump sum investment is overwhelmingly the rational decision… but I digress). Now you are stuck managing this DCA plan over the next 6/12/18/24/infinity months, always with the threat of the advisor or client getting cold feet and pulling the plug on the whole plan because markets are hitting new highs or new lows or whatever.

One idea I have been toying with is parking those DCA assets into one of these buffer products. Depending upon your specified horizon, you could ladder specific tranches out to their scheduled deployment date using the defined horizon offerings (like Innovator’s JZAN product which offers 100% downside protection from January of one year to January of the next with the opportunity of ~7% upside participation). There are also 6month- and quarterly-resetting offerings in the Innovator suite which could be used to more precisely match DCA schedules. There are obviously increasingly more options available in this space as time goes on, so pick the most fitting offering for your use case, I’m just the most familiar with Innovator and it’s sort of become their bread and butter.

https://www.innovatoretfs.com/pdf/100_buffer_investor_guide.pdf Innovator’s current offerings as of 2/28/25

I really like this approach and I think it will resonate with clients/investors because you’ve still got your DCA plan in place, but the buffers offer some upside participation that you otherwise wouldn’t achieve in a cash sweep or money market vehicle. If you hit the upside cap on the buffer you would, of course have been better off just having been fully invested from the outset, but YOU the investment professional already knew that. At least this way you can offer a “have your cake and eat it too” solution for clients.

https://www.innovatoretfs.com/pdf/100_buffer_investor_guide.pdf 100% buffer scenarios

Of course if you are willing to accept some small losses in exchange for more upside, you could venture into the true “buffer” offerings, which offer some smaller level of protection (protection against the first 9% drawdown, participation in the first -5% but then protected down to -35%, etc - there are a number of different configurations to choose from). But I guess I’d argue at that point if you are just splitting hairs on how much downside exposure you (or the client) want, then why aren’t you just putting the money to work right away to begin with and be done with it?

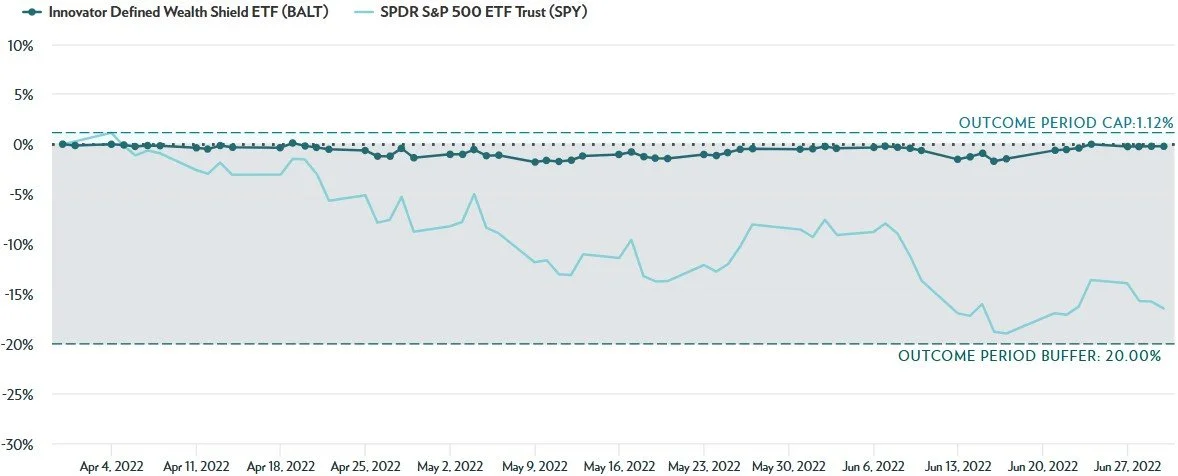

BALT, the “Defined Wealth Shield ETF” might be the lightest lift from an operational perspective. It’s got a quarterly reset with a full 20% buffer, meaning each quarter you just need the S&P to fall less than 20% to maintain your full principal. Then the protection rolls over to the next quarter. For our DCA use case, you can just drop all your assets in at the beginning then sell your tranche amounts out at each quarterly reset (or, say, monthly if you are on a more granular DCA plan). One of the nice things about the ETF implementation here is that there is daily liquidity, even when you are between the reset periods. I suppose the one caveat to point out here is that there’s no universal law dictating that you can’t lose principal here. The ETFs can and do trade below their buffer amount intra-reset period, albeit not by significant amounts.

Consider BALT’s performance in the teeth of a gnarly year like 2022. In the biggest down quarter (Q2) BALT traded at a max of about -1.8% about a third of the way through the quarter (i.e. had breached it’s buffer intra-reset period by ~2%). This was as the S&P was down 13% since the start of the Q.

https://www.innovatoretfs.com/define/previous/ for BALT 4/1/22-6/30/22

So it’s not as if you won’t see some price fluctuation, but not a ton. Plus, by the end of the outcome period the price will grind back to flat (assuming you don’t breach the bottom of your buffer). I point this out because if you, like shops I have worked at before, use a drawdown trigger to accelerate these DCA tranches you would like to make sure as much of your principle is can be deployed as possible.

I could go on about some of the pitfalls, trade offs, and additional considerations. Do not consider this a simple, silver-bullet solution. You should think carefully about the implications of this novel twist on a vanilla DCA strategy and whether it makes sense for you/your clients’ situation and objectives. But I do think there is something compelling here and I would love to hear any improvements or suggestions you might have.