Catastrophe Bonds: A New Asset Class

by HunterOne topic I have been obsessed with lately is catastrophe bonds. For the uninitiated, catastrophe bonds (cat bonds) are specialized risk-linked securities designed to transfer specific catastrophe and natural disaster risks (wind damage, earthquakes, floods, etc.) from insurers to capital market investors. Originating in the mid-1990s following major events like Hurricane Andrew and the Northridge earthquake, these financial instruments emerged as an innovative way for insurers to manage potential large-scale losses. Cat bonds have also begun to expand to cover a broader range of risks, including life insurance risks, third-party liability, terrorism, and financial guarantees. The primary purpose remains providing insurers access to capital markets for effective risk transfer and financial protection against major catastrophic events.

The typical structure involves a special purpose vehicle (SPV) that issues securities to investors, who receive attractive returns in exchange for assuming potential catastrophe risk. Investor capital is held by a third-party trustee for the duration of the bond’s life (typically ≤ 3yrs). One of the attractive aspects of cat bonds is the dual yield component: namely the risk spread paid by the issuer (effectively premiums paid to the investors/bondholders) plus the “risk free” base rate that the trust assets generate while being held by the trustee. These bonds have specific trigger conditions that determine when investors might lose some or all of their principal, such as actual losses experienced, industry-wide loss thresholds, or parametric disaster conditions.

SwissRe maintains the oldest and most widely-available index (SwissRe Global Cat Bond Index) that I have been able to find. Here are the annual returns for the index since 2007(when the indexes launched, however there is data back to 2002 if you are so inclined). Images courtesy of Amundi/Pioneer:

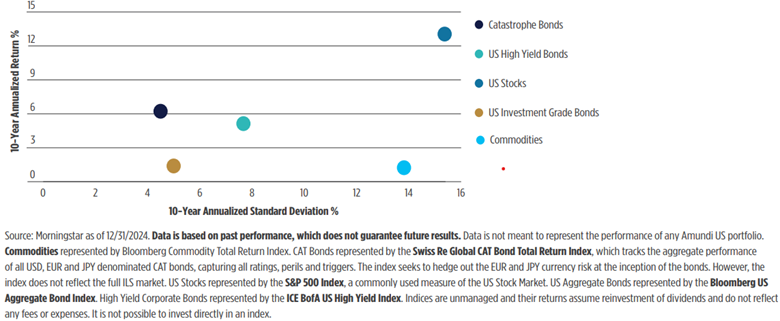

Annualized returns of ~6% over almost two decades aren’t too shabby. Here’s the risk/return profile relative to other major asset classes as of 12/31/24 (again, courtesy of Amundi/Pioneer):

Again, looks pretty attractive to me. Annualized returns that exceed US fixed income markets with less “volatility.” I quotate because I fully recognize some element of “volatility laundering” here. But before we get to that I want to drive home the real kicker here, which is the correlation profile of cat bonds (again courtesy of Amundi/Pioneer):

As you can see, they show little correlation to other major (U.S.) investment assets. And this is the real game changer to me; I fundamentally understand why there is no correlation to broader financial markets. Hurricanes in Florida and earthquakes in Japan obviously have some regional/local economic impact, but a single natural catastrophe should not bring down the global financial system. And yet there is completely reasonable economic rationale for people and businesses to seek insurance against those risks, insurers to meet those needs while offloading some of that risk elsewhere, and objective third party investors who seek an uncorrelated stream of attractive returns. The more and more I dive into the mechanics of these instruments, the more cat bonds look like a win-win for all parties involved.

Looking at the macro picture here, a 2023 report from McKinsey shows an increasing frequency and cumulative financial impact of disasters in the U.S. over the last few decades:

While a 2024 report from Deloitte claims that “economic losses from natural catastrophes reached US$357 billion in 2023 globally. Yet only 35% of these losses were insured, leaving a protection gap of 65% or US$234 billion.” And while that might sound alarming, they go on to point out that these insurance coverage gaps are even wider outside of the U.S.

Several tough years for the insurance industry and increasingly persistent levels of inflation have put significant upward pressure on renewal rates over the last few years as insurers increasingly need to offset inflated replacement costs and compensate for increasing uncertainty around frequency and severity of catastrophic events. While reinsurers represent several hundred billions of dollars worth of capacity, what I see here is a growing need and a steadily increasing appetite from investors. Total catastrophe bond and insurance-linked securities (ILS) capital outstanding has grown from $5.2 billion two decades ago to nearly $50 billion as of year end 2024 (~12% CAGR), according to data from Artemis.

All of these elements of the equation make total sense to me: increasing need for capital, growing familiarity and logical portfolio fit for investors, increasingly established infrastructure for issuance of securities, the economic and prudent spreading of risk amongst industry and investors, etc. And they all point to one thing - catastrophe bonds (and perhaps more broadly ILS in general) will and should become an institutionalized asset class. To be honest, if I were a few years younger I would be figuring out how to break into catastrophe/ILS and trying to ride the wave of asset growth similar to what we are seeing in private credit now.

So from an allocator angle, what is there to be done here? Assuming you are ready to dive deeper into this space, there is some good news. While there are many private vehicles available for cat/ILS exposure in investors’ portfolios, there are a few public/semi-liquid/liquid options. StoneRidge’s High Yield Reinsurance Risk Premium Fund (SHRMX, SHRIX) is structured as an interval fund and offers globalized cat bond exposure. Amundi’s Pioneer CAT Bond Fund (CBYYX, ACBAX, ACBKX) is structured as a true-blue daily liquid mutual fund that specifically focuses on the more liquid segments of cat bond markets. Also in the fully liquid structure is the kind of odd Ambassador Fund from Embassy Funds. I can’t seem to find much info on this one, but it does offer a cat bond portfolio, albeit it appears to be limited to institutional access at the big brokers. Tread with care on that one. After some delays, there also appears to be a Brookmont Catastrophe Bond ETF (ticker ILS) on the way with an imminent launch date.

I should mention at this point that the one stop shop for all things catastrophe is Atermis, run by Steve Evans. I’ve found it to be an incredible resource for getting up to speed on what I see as the next burgeoning asset class in financial markets. Anything and everything you could possibly want or need is there and I encourage interested readers to check it all out.

Hopefully this was a good, quick primer for readers. This will undoubtedly not be the last time I cover cat bonds on the blog, though. So, more to come.